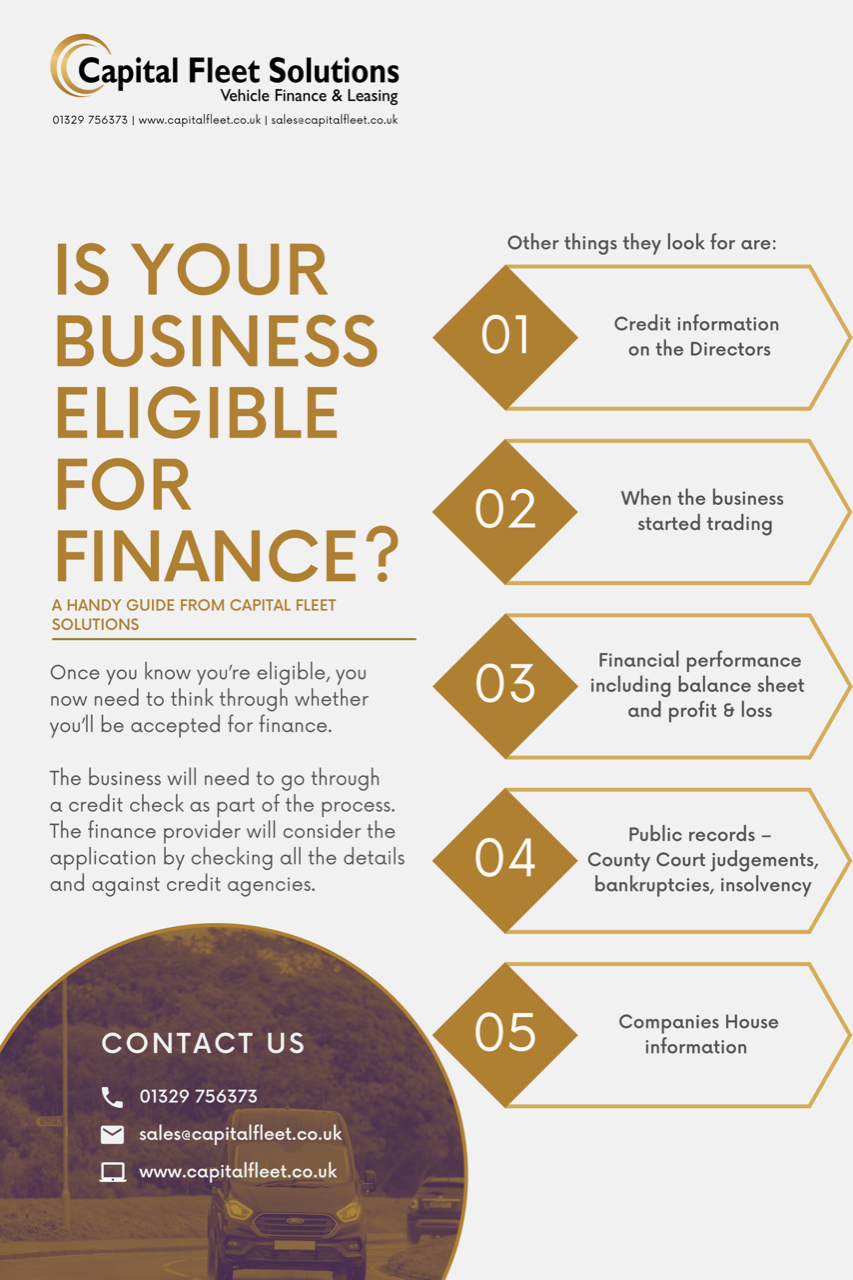

Personal Finance Leasing

Contract Hire or Finance Lease?

Many people assume that lease contracts are the same and only concern themselves with the bottom line. However, there are two different types of lease options.

These are Contract Hire and Finance Lease. Both types may seem similar on paper but on closer inspection there are different financial implications that you need to be aware of before opting for either.

Contract Hire

By far the most common form of lease agreement is Contract Hire. This option allows you to choose the vehicle you want and pay a set monthly fee to use the vehicle for an agreed period and mileage allowance. Tax, maintenance and breakdown cover are often included leaving you with peace of mind when driving your vehicle.

At the end of the agreed rental period the vehicle is returned to the leasing company. The lessee is not responsible for the disposal or sale price of the vehicle – making it a very easy and risk-free way to run a vehicle.

Contract hire rentals are designed to cover the depreciation costs of the vehicle over the term of the agreement plus interest, but not the full cost of the vehicle. The rental cost is based on:

- The price of the vehicle excluding VAT

- Interest is added to the ex-VAT price of the vehicle and the balance, minus the leasing company residual value risk / balloon payment, which is paid over a fixed period.

- The rentals will attract VAT at the current rate.

Deposits are not taken however, advance rentals are usually required at the start of the agreement.

Providing the vehicle is returned without damage at the end of the contract and within the set mileage there should be no problems or further charges. If the vehicle has exceeded the agreed mileage, then a pence per mile charge plus VAT will apply to each mile over the contracted amount. This mileage charge is agreed in advance so you know what the amount will be. The leasing company could also charge a compensation payment if the vehicle has not been maintained or serviced according to the manufacturer’s recommendations. Damage charges are raised in-line with the BVRLA return guidelines.

A contract hire agreement can be settled at any point during the agreement. However, there could be penalties for doing this which will be detailed in the agreement. You may also have the option to extend the length of the contract past the Primary Period of Hire. There may be a change in the rental amounts for this additional period.

It’s easy to think you have spotted a great deal and sign up without knowing about a lesser well-known option that could actually reward you financially – Finance Lease.

Finance Lease

Finance Leasing like contract hire, allows you to rent a vehicle for your business. This is great option for VAT registered businesses. VAT is paid on the monthly rentals and is reclaimable for those who are VAT registered. Also, there are no mileage restrictions which can make this an attractive option if your job involves spending lots of time on the road.

Finance leasing is a flexible leasing option which gives you the use, but not the ownership, of a vehicle. As with Contract Hire you pay an agreed monthly rental which is determined by the initial cost of the vehicle, how long the lease will last for, the overall value and the end balloon payment.

The usual length of agreements (the primary period of hire) is between two and five years. Deposits are not taken under a Finance Lease however, advance rentals are usually paid at the start of the agreement. The minimum and maximum advance rentals are determined by the individual lender. However, three months advance rentals is a common amount.

One of the main differences with Finance leasing is what happens at the end when the vehicle is sold - the customer gets the opportunity to:

- Return the vehicle to the leasing company who will sell it and refund any surplus.

- Sale proceeds to the customer as a rebate of rentals (this figure is usually around 95%-99% of the surplus sale proceeds with some of the surplus being retained. by the lease company to cover administration costs).

- Arrange for the sale of the vehicle to an `independent third party`. The lease company would receive the full sale proceeds and refund the customer a fixed percentage (as above) of any surplus that is generated as a rebate of rentals. For example, if you can sell the van for a higher price due to a better condition or lower mileage, then you receive the difference.

- Continue to use the vehicle for as long as they want on payment of an annual secondary period rental (commonly known as a peppercorn rental). Alternatively, the customer could choose to purchase the vehicle at a bargain purchase price – so it could be used as an economic way to acquire a vehicle if you didn't want to commit to years of leasing a van.

With a Contract Hire agreement you will always have to hand the vehicle back to the leasing company.

So whats the best option for me?

Not everyone is going to run their van into the ground. With Finance Lease you have far more control over how you manage your van and will reap the benefits over the longer term. With the more common Contract Hire, you are simply paying for the privilege of looking after your van for which you will receive no reward at the end of the lease.

Ultimately, the choice is yours and we always recommend you seek professional advice before making any final decisions.

If you need further information or require comparative quotes on both finance options please call on 01329 756 373 or Enquire Here